LIFO Explained: Meaning, Formula, Example & Key Advantages

Learn what LIFO (Last In First Out) in inventory management means, how it works with examples, its advantages, disadvantages, and differences from FIFO in simple terms.

What Does LIFO in Inventory Management Mean?

LIFO (Last In, First Out) is an inventory valuation method where the most recently purchased or produced items are sold first.

In simple terms:

The newest stock goes out first, and the older stock stays in inventory.

Why Is LIFO Important?

LIFO directly affects:

Cost of Goods Sold (COGS)

Profit margins

Taxes

Financial reporting

Because newer items are usually more expensive (due to inflation), LIFO can significantly change how profitable a business appears on paper.

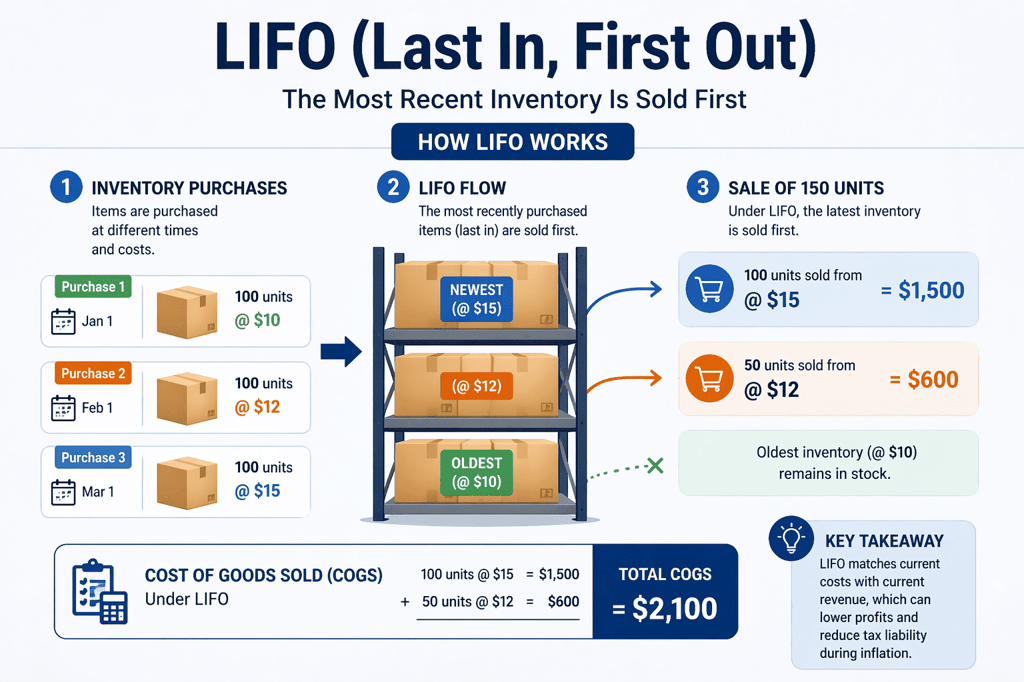

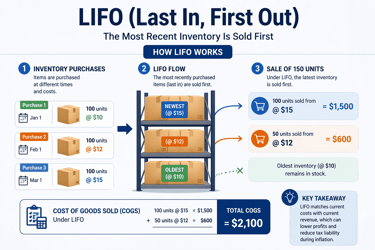

How LIFO Works (Simple Explanation)

Imagine a warehouse where items are stacked one over another.

The latest stock is placed on top

When a sale happens, the top items (newest) are sold first

This is exactly how LIFO operates.

LIFO Formula

To calculate cost under LIFO, businesses use this basic approach:

COGS=Cost of most recent inventory sold first

In practice:

Start from the latest purchase

Move backward until all sold units are accounted for

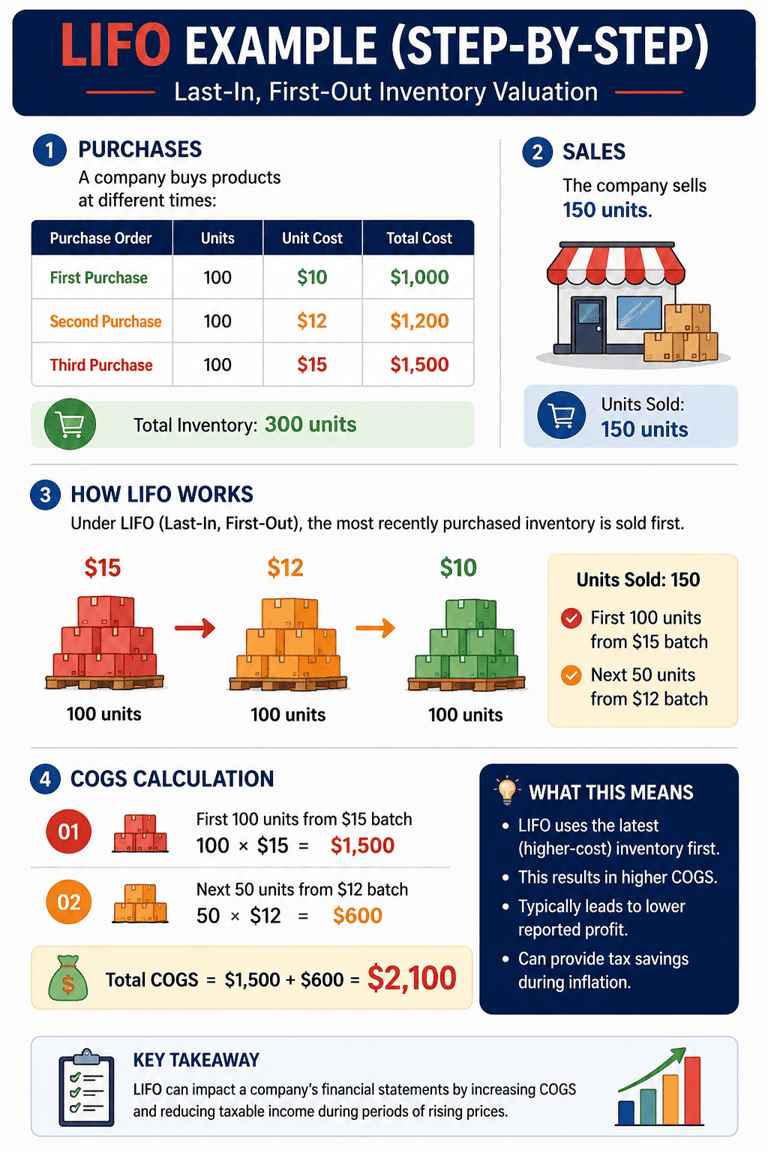

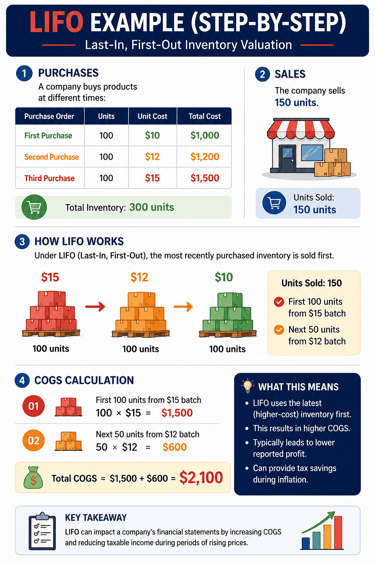

LIFO Example (Step-by-Step)

Let’s say a company buys products at different times:

100 units @ $10

100 units @ $12

100 units @ $15

Now, the company sells 150 units.

Under LIFO:

First 100 units → from $15 batch

Next 50 units → from $12 batch

COGS Calculation:

(100 × $15) = $1500

(50 × $12) = $600

👉 Total COGS = $2100

LIFO vs FIFO (Quick Insight)

While LIFO sells the newest inventory first, FIFO (First In, First Out) does the opposite.

LIFO → New stock sold first

FIFO → Old stock sold first

This difference leads to:

Higher costs (LIFO)

Lower reported profits during inflation

Advantages of LIFO

1. Tax Benefits (in inflation periods)

Since newer inventory costs more:

COGS increases

Profit decreases

Taxes reduce

👉 This is why some companies prefer LIFO.

2. Matches Current Costs with Revenue

LIFO uses recent prices, making financial results more aligned with current market conditions.

3. Better for Certain Industries

LIFO can work well in industries where:

Prices rise frequently

Inventory costs fluctuate a lot

Disadvantages of LIFO

1. Not Allowed Globally

LIFO is not permitted under IFRS (International Financial Reporting Standards)

👉 It is mainly used in:

The United States (under GAAP)

2. Old Inventory Stays on Books

Older inventory remains unsold in accounting records, which can:

Distort inventory value

Make balance sheets less realistic

3. Lower Profit Reporting

Because costs are higher:

Profits appear lower

This may not look attractive to investors

Where Is LIFO Used?

LIFO is commonly used in industries such as:

Retail chains

Manufacturing

Automotive parts

Commodities businesses

These sectors often deal with:

Price fluctuations

Large volumes of inventory

When Should Businesses Use LIFO?

LIFO is suitable when:

Prices are rising (inflation)

The company wants to reduce tax liability

Inventory turnover is high

However, it may not be ideal for:

Global companies (due to IFRS restrictions)

Businesses that want higher reported profits

Real-World Perspective

Even though LIFO is still hanging around in some regions—mainly under GAAP—most global companies steer clear of it. And honestly, there are some pretty practical reasons why.

For starters, LIFO isn’t allowed under IFRS, which is the accounting standard used in most countries. So if a company is working internationally or planning to expand, sticking with LIFO can cause compliance headaches. In some cases, they’d even have to juggle two sets of financial records, which is as messy and time‑consuming as it sounds.

Another issue is how LIFO messes with financial comparisons. Because it uses the most recent (and usually higher) costs during inflation, profits look smaller on paper. Sure, that might help with taxes, but it makes it tough for investors and stakeholders to compare performance across companies—or even across different years. In plain English, the numbers don’t always tell a consistent story.

Then there’s the operational side. LIFO doesn’t really match how inventory flows in real life. Most businesses—especially in retail, food, or pharma—sell older stock first. Using LIFO in the books while moving inventory differently in practice can create confusion in tracking and reporting.

That’s why many companies lean toward FIFO or weighted_average methods. They’re simpler, globally accepted, and give financial statements that are clearer and easier to compare. Over time, that kind of transparency and ease of management makes a big difference.

Common Mistakes to Avoid

Confusing physical flow with accounting method

(LIFO is often used only for accounting, not actual movement)Ignoring regulatory restrictions

(LIFO is not allowed in many countries)Not analyzing impact on tax and profit

Final Thoughts

LIFO is a powerful inventory valuation method that can significantly influence a company’s financial performance. By selling the most recent inventory first, it helps businesses manage costs and reduce taxes during inflationary periods.

However, it comes with limitations—especially in global reporting standards—and may not be suitable for every business.

If you’re laying the groundwork in supply chain or accounting, it’s worth knowing both LIFO and FIFO. These two methods aren’t just technical jargon—they’re the core of how businesses value inventory. Understanding the differences between them gives you a clearer picture of how companies track costs, report profits, and make strategic decisions. Together, they form the backbone of inventory valuation strategies that industries everywhere rely on.