FIFO vs LIFO in Inventory Accounting: Differences, Benefits & Real Examples

Confused about FIFO vs LIFO in accounting? Learn key differences, real examples, advantages, and choose the best inventory valuation method for your business.

What is FIFO (First-In, First-Out)?

FIFO assumes that the oldest inventory items are sold or used first. In other words, the first products you purchase are the first ones to leave your inventory.

Example of FIFO

Let’s say a company purchases inventory in the following order:

100 units at $10 each

100 units at $12 each

If the company sells 100 units, under FIFO:

The cost of goods sold (COGS) = 100 units × $10 = $1,000

Remaining inventory = 100 units at $12

Key Characteristics of FIFO

Inventory reflects recent (current) prices

COGS reflects older (historical) costs

Often aligns with the physical flow of goods (especially perishable items)

What is LIFO (Last-In, First-Out)?

LIFO assumes that the most recently purchased inventory is sold first. The latest items added to inventory are the first ones to be used or sold.

Example of LIFO

Using the same data:

100 units at $10 each

100 units at $12 each

If the company sells 100 units, under LIFO:

COGS = 100 units × $12 = $1,200

Remaining inventory = 100 units at $10

Key Characteristics of LIFO

Inventory reflects older (historical) costs

COGS reflects recent (current) costs

Often used for financial and tax benefits in certain regions

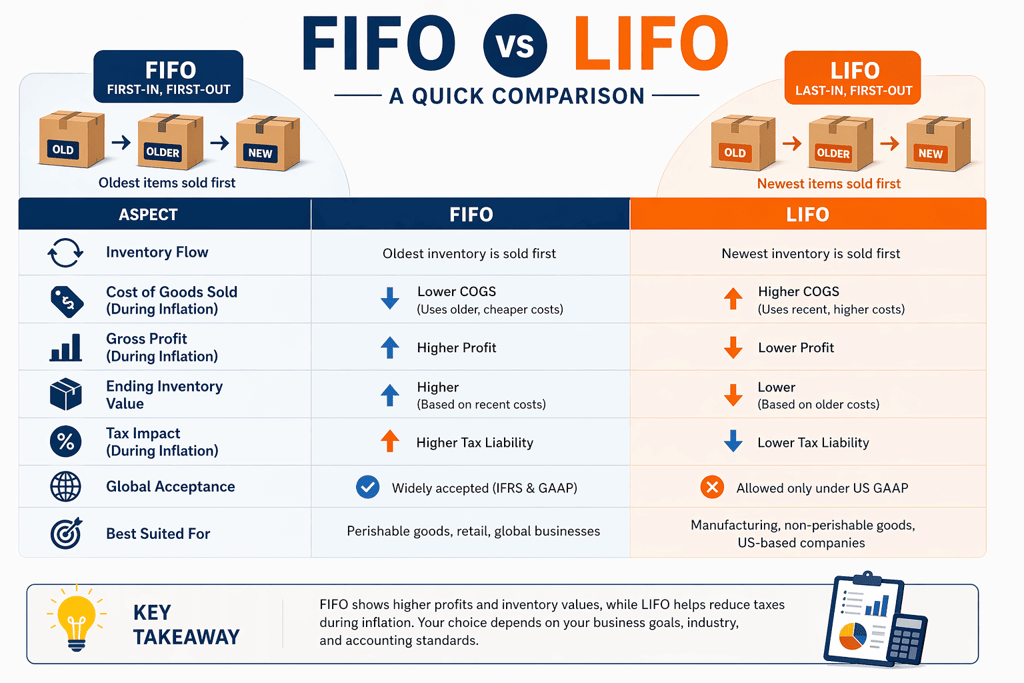

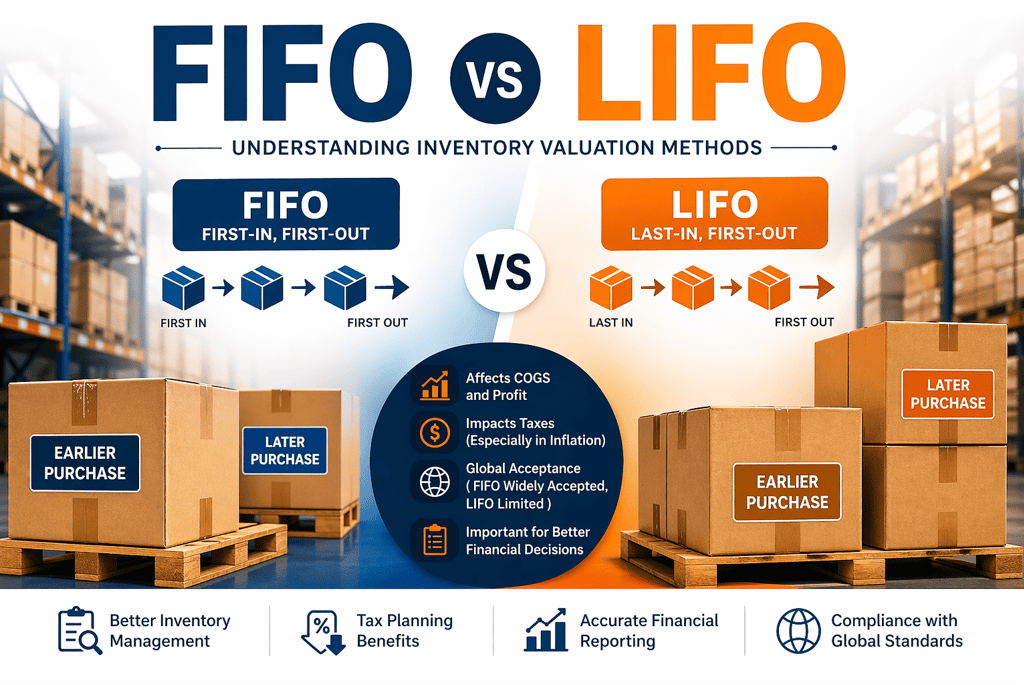

FIFO vs LIFO: Key Differences

Impact of Inflation

The difference between FIFO and LIFO becomes more significant during inflation (when prices are rising).

Under Inflation:

FIFO:

Uses older, cheaper costs for COGS

Results in higher profit

Leads to higher taxes

LIFO:

Uses recent, higher costs for COGS

Results in lower profit

Leads to lower taxes

This is one of the main reasons companies choose LIFO where it is allowed.

Global Accounting Perspective

One critical factor to understand is that LIFO is not permitted under International Financial Reporting Standards (IFRS), which are used in most countries worldwide.

FIFO is accepted globally under both IFRS and GAAP

LIFO is allowed under US GAAP, but not under IFRS

What this means:

Companies operating internationally typically use FIFO

Multinational firms often avoid LIFO to maintain consistency across countries

Advantages of FIFO

1. Better Reflection of Inventory Value

Ending inventory is based on recent costs, making it closer to current market value.

2. Simplicity and Logical Flow

FIFO aligns with the natural movement of goods, especially in industries like food, pharmaceuticals, and retail.

3. Higher Profit Reporting

During inflation, FIFO results in higher profits, which can be beneficial for investors and stakeholders.

Disadvantages of FIFO

1. Higher Tax Burden

Higher profits mean higher taxable income.

2. Less Matching of Current Costs

COGS reflects older costs, which may not match current revenue levels.

Advantages of LIFO

1. Tax Benefits

Lower profits during inflation lead to lower taxes.

2. Better Matching Principle

COGS reflects current costs, providing a more realistic view of profitability.

Disadvantages of LIFO

1. Not Globally Accepted

LIFO is banned under IFRS, limiting its use internationally.

2. Outdated Inventory Valuation

Ending inventory may be valued at very old costs, making balance sheets less realistic.

3. Complexity

Maintaining LIFO layers can be complicated, especially for large inventories.

Where this is getting applied?

FIFO is commonly used in:

Retail (e.g., supermarkets)

Food and beverage industries

Pharmaceuticals

E-commerce businesses

LIFO is often used in:

Manufacturing companies (in the U.S.)

Industries dealing with non-perishable goods

Businesses looking to reduce tax liability during inflation

📦 Real-World Example: FIFO vs LIFO (Amazon Warehouse)

🟢 FIFO Example (What Amazon Mostly Follows)

Imagine Amazon stores wireless headphones in its warehouse:

January stock: 100 units at ₹1,000 each

February stock: 100 units at ₹1,200 each

Now, a customer places an order for 150 units.

👉 Using FIFO:

First 100 units sold from January stock (₹1,000)

Next 50 units sold from February stock (₹1,200)

Result:

Cost of Goods Sold (COGS) is lower

Remaining inventory is valued at newer (higher) cost

Products shipped are older stock → better for avoiding dead stock

📌 This is ideal for Amazon because it deals with fast-moving and sometimes perishable or trend-sensitive products.

🔴 LIFO Example (Hypothetical Scenario at Amazon)

Using the same example:

January stock: 100 units at ₹1,000

February stock: 100 units at ₹1,200

👉 Using LIFO:

First 100 units sold from February stock (₹1,200)

Next 50 units sold from January stock (₹1,000)

Result:

Higher COGS (because recent stock is more expensive)

Lower profit (useful for tax savings in some countries)

Older inventory (January stock) remains in warehouse → risk of obsolescence

📌 This is not ideal for Amazon’s model, as unsold older items can lead to:

Product damage

Expiry (for certain categories)

Customer dissatisfaction

⚖️ Key Takeaway (Amazon Context)

Amazon primarily operates closer to FIFO in practice

This ensures:

Faster inventory turnover

Better customer experience

Reduced waste and storage costs

Which Method Should You Choose?

At the end of the day, whether you go with FIFO or LIFO really comes down to timing, the type of items you’re dealing with, and what makes the most sense for your business. There’s no one‑size‑fits‑all answer—it’s about picking the method that fits your situation best.

Choose FIFO if:

You operate globally

You want accurate inventory valuation

You deal with perishable goods

You follow IFRS

Choose LIFO if:

You operate in the United States

You want to reduce taxable income

Your inventory costs are rising significantly

FIFO vs LIFO: Quick Summary

FIFO sells older inventory first → Higher profits, higher taxes

LIFO sells newer inventory first → Lower profits, lower taxes

FIFO is globally accepted → LIFO is restricted

FIFO shows realistic inventory value → LIFO focuses on tax efficiency

Final Thoughts

FIFO and LIFO are more than just accounting methods—they directly impact how businesses report profits, manage taxes, and present financial health.

For a global audience, FIFO is generally the preferred and more practical method, given its widespread acceptance and alignment with real-world inventory flow. However, LIFO still plays a strategic role in regions like the United States, especially for companies looking to manage tax exposure during inflationary periods.

Understanding both methods allows businesses to make informed decisions that align with their operational, financial, and regulatory needs.

If you're building expertise in supply chain or planning to optimize your inventory strategy, mastering concepts like FIFO and LIFO is a strong foundation for long-term success.